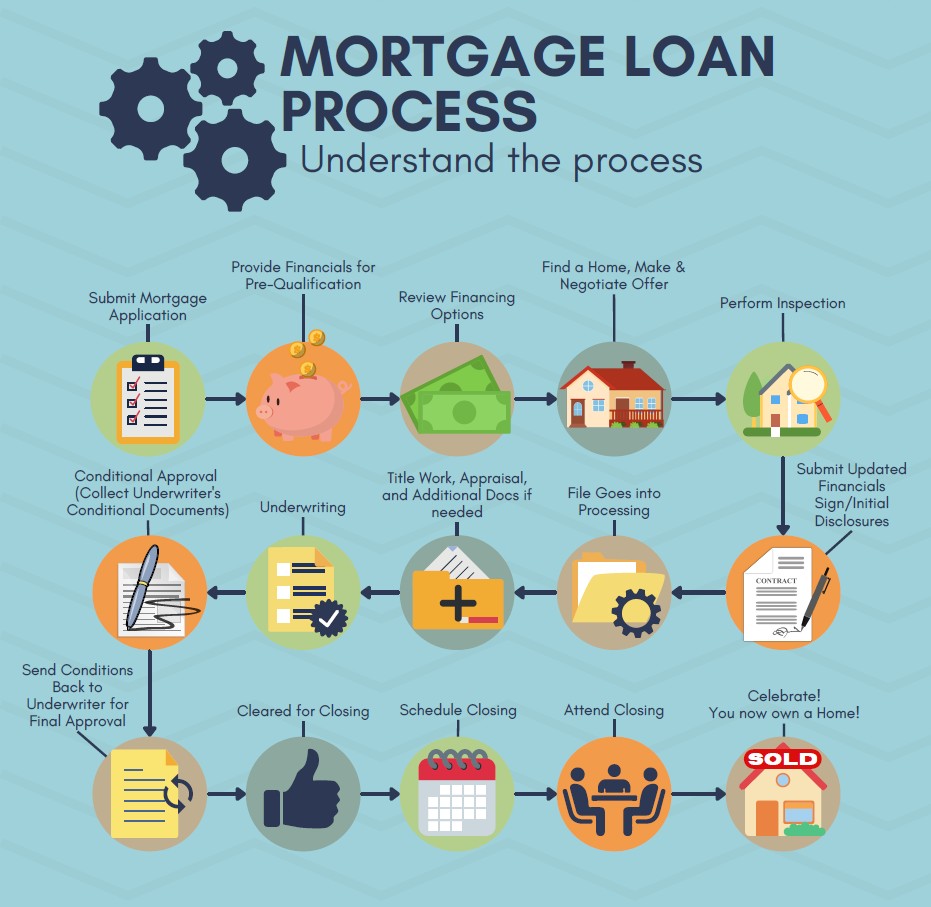

🔄 OUR PROCESS

A simple, straightforward process

Step 1: Start the conversation

We’ll talk through your goals, your situation, and what you’re trying to accomplish.

What to expect: A short phone or video call to understand your timeline, budget, and priorities.

Step 2: Explore your options

We’ll walk you through what’s available—clearly and honestly—so you understand what actually fits.

What to expect: Clear explanations of loan types, rates, terms, and tradeoffs so you can compare options.

Step 3: Choose with confidence

No pressure. Just guidance so you can make the best decision for you.

What to expect: Recommendation of one or two best-fit options and a straightforward summary of next steps.

Step 4: Move forward smoothly

We handle the details, keep you updated, and make sure nothing falls through the cracks.

What to expect: Paperwork coordination, checklist tracking, and regular status updates until closing.

Step 5: Close and beyond

We’re here through closing—and after. Questions don’t stop once the paperwork is signed.

What to expect: Post-close support, answers to follow-up questions, and resources for homeownership.

Simple. Clear. No surprises.

Frequently asked questions

Home buyers & Refinance clients

What documents will I need to start?

Common documents include photo ID, recent pay stubs, W-2s or tax returns (typically 2 years), recent bank statements, and information about debts and assets. For self-employed borrowers, profit-and-loss statements and additional tax documents may be required.

How long does the mortgage process usually take?

From application to closing typically 30–45 days for purchase loans, sometimes shorter for simple refinances. Time depends on appraisal scheduling, underwriting, and how quickly documents are provided.

Will shopping for rates hurt my credit?

Rate shopping within a short window (usually 14–45 days, depending on the scoring model) is treated as a single inquiry for mortgage credit scoring. We’ll explain the best timing before you lock a rate.

Should I refinance now or wait?

That depends on your goals—lower monthly payment, shorten loan term, switch to a fixed rate, or cash-out. We’ll run scenarios showing break-even points and long-term savings to help you decide.

What is the difference between prequalification and preapproval?

Prequalification is an initial estimate based on self-reported info. Preapproval requires documentation and a credit check and gives sellers stronger evidence of your ability to close.

How much will I need for a down payment and closing costs?

Down payment requirements vary by loan type (as low as 0–3% for certain programs). Closing costs commonly range from about 2–5% of the loan amount. We’ll provide an itemized estimate early in the process.

Can I get mortgage help if I have less-than-perfect credit?

Possibly. There are programs and strategies for different credit profiles. We’ll review options and, if needed, steps to improve your profile before applying.

What happens after closing if I have questions?

We remain available after closing for questions about payments, escrow, or future refinancing. Our goal is to support you through and beyond the transaction.

Compliance: This material is for informational purposes only and does not constitute legal, financial, or tax advice. All loans are subject to credit and underwriting approval. Terms, conditions, and availability are subject to change without notice.

2026 Link Mortgage. All rights Reserved